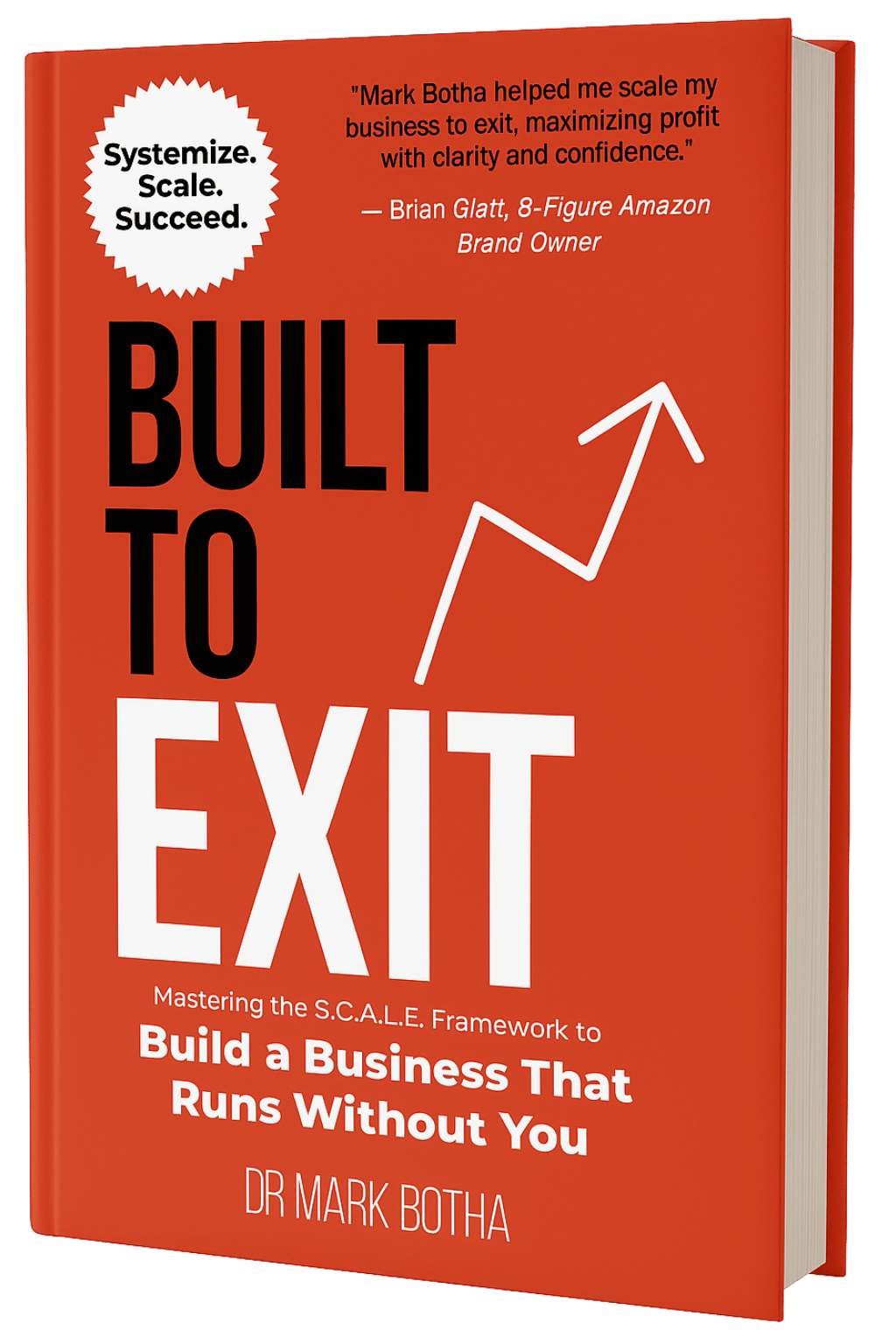

Build a Business That Runs Without You and Sells for What It’s Really Worth

Most founders set out to build freedom and end up with a very demanding job. The Exit Academy is the operating system for the other path: the S.C.A.L.E. Framework that turns a founder-dependent business into a scalable, sellable asset.

Choose Your Next Move:

Not sure where you stand? Download the free 3-minute FREE Exit Scorecard first.

The framework

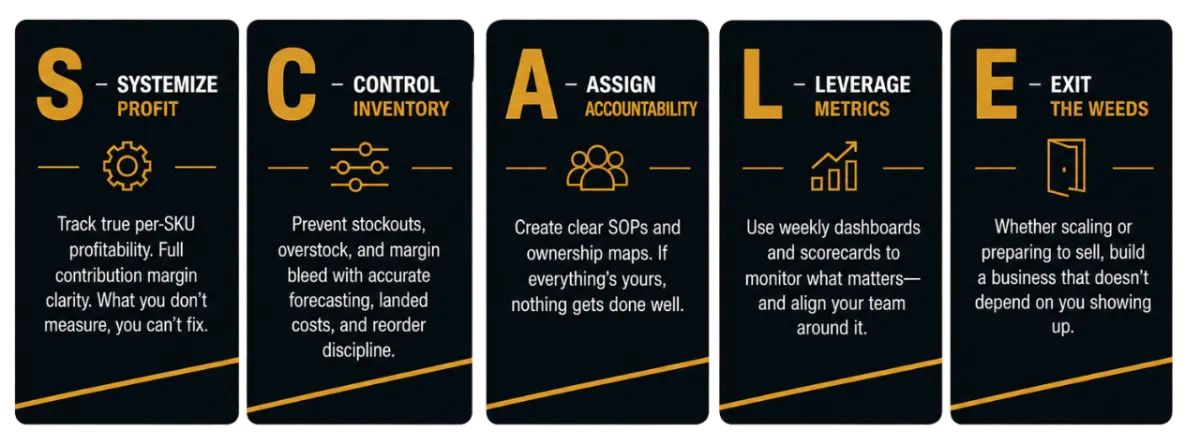

The S.C.A.L.E. Framework is a proven system for a business that works

with you or without you

⭐⭐⭐⭐⭐ 5.0 / 5 — 225+ Goodreads ratings

A practical, no-fluff system for building a commerce business that operates smoothly, profitably, and independently of its founder. Whether your goal is a future sale, smarter expansion, or simply getting your life back, this is the blueprint for designing a company that doesn’t need you in every decision.

It’s the same framework taught inside the Exit Academy and it starts in the book, Built to Exit.

The Hard Truth

Most founders don’t own a scalable company. They own a very demanding job.

If your business can’t run without your constant involvement, leans on you for every major decision, and grows revenue but not freedom — then the longer it goes on, the harder it becomes to step away or sell.

Real founders. Real numbers.

Join The Academy to learn what changes when the systems carry the load instead of you.

TESTIMONIALS

Real founders. Real progress.

From executive pivots to business breakthroughs, our coaching and community help members build structured, scalable businesses — built to exit.

I came in thinking I had a $3M business. Eighteen months into the S.C.A.L.E. work, a buyer valued us at nearly double — not because revenue jumped, but because the business finally ran without me. The Academy turned my 'job' into an actual asset.

James Walter

Founder, 8-figure DTC Brand

I hadn't taken a real two-week holiday in six years. I just got back from one, and the team didn't call me once. That's what the Academy actually sells — not tactics, but the day the business stops needing you in the room.

Chloe Maddox

Founder, Meta Agency

We closed the sale last quarter. The diligence process that terrifies most founders was almost boring — our financials, SOPs, and ownership were already clean because that's what the Academy makes you build from day one. I exited on my terms.

Jason Pena

Founder, Shopify Brand

I'd read the books and joined the groups. The difference here was the room — operators who'd actually exited, telling me exactly which fires to stop fighting. I stopped being the bottleneck within ninety days. Everything compounded from there.

Beth Anderson

Founder, Amazon Private Label Brand

The Real Problem

You’re not stuck because you lack ambition. You’re stuck because the

business still runs through you.

When every escalation, approval, and operational fire lands back on your desk, the company hasn’t become scalable. It’s become dependent.

That’s not a founder weakness. It’s an operational design problem.

Most commerce businesses between $2M and $5M hit this exact wall. The systems that created early growth become the very things capping your scale, your freedom, and your exit value.

⭐⭐⭐⭐⭐ 5.0 / 5 — 225+ Goodreads ratings

Five Disciplines

The S.C.A.L.E. Breakdown

Five disciplines. One business that runs itself.

The Academy brings together founders on the same journey — resources, real discussion, and

experts who help you build a business that supports your life instead of consuming it.

The Community

Learn + Community = Scalable Growth

Inside the Exit Academy you combine expert learning with a curated network of commerce operators. You get tailored support, peer-driven insight, and an environment built to move you from founder-dependent to exit-ready — faster than you would alone.

What is your annual profit? Most founders leave more on the table than they realize!

$0

Drag the slider to see your estimate

⭐⭐⭐⭐⭐ 5.0 / 5 — 225+ Goodreads ratings

the exit accademy

Real business growth isn’t about doing more, it’s about building systems that work without you.

Join a private network of commerce founders building businesses that are scalable, profitable, and ready to sell — on their terms.

THE COMMUNITY

A community engineered for scalable growth

Breakthroughs come faster with the right people around you. The Academy is a curated room of operators who’ve faced what you’re facing.

Mastermind sessions

Solve real challenges with peers who get the founder’s seat — in hours, not months.

"Highly recommend this"

Coaching & workshops

Monthly working deep-dives on scaling and exit — sessions that drive action, not passive webinars.

"Highly recommend this"

A supportive operator network

Ongoing accountability with founders committed to growth — curated for quality, not noise.

"Highly recommend this"

Exclusive content & insights

Early access to frameworks, guest experts, and case studies and playbooks.

"Highly recommend this"

THE STORIES BEING BUILT HERE

Four founders. Four turning points.

These are the kinds of breakthroughs members are working toward inside the Academy — each one a different stage of the same journey.

THE OPERATIONAL WIN

“I finally got out of the day-to-day.”

I came in drowning. Every fire ended on my desk, and I'd convinced myself that was just what owning a business looked like. The first 90 days inside the Academy weren't about exit strategy — they were about basic operating discipline. SOPs, ownership maps, a leadership layer that actually decides things. By month four, I was off three group chats and the team didn't notice. That was the moment I knew it was working.

Andre Frank

Operational breakthrough

Exit Academy Member

THE EXIT

I’d been told I had a $4M business. I never quite believed it — the buyer in my head always assumed there was a catch. The Academy made me build the company a buyer would actually pay a premium for: clean financials, documented systems, ownership that didn’t live in my inbox. When the offer came, due diligence was almost boring. We closed for a number I didn’t think was possible eighteen months earlier.

Ava Cooper

Successful Exit

Member

THE SCALE-UP

“Revenue doubled. My hours didn’t.”

I joined because I wanted to grow, not because I wanted to sell. What I didn’t expect was that building ‘as if you might sell’ was the fastest way to scale. The S.C.A.L.E. work forced me to find the actual margin in my SKUs, hire the leadership I’d been avoiding, and stop treating my business like a hobby with a payroll. Revenue is up over 80% this year. My hours are not.

Liam Thompson

Scaling Stage

Active Member

THE MINDSET SHIFT

“I stopped building a job.”

I’m not planning to sell. Maybe ever. But the way I think about my company is completely different now. Every decision goes through one filter: does this make the business more dependent on me, or less? That single question changed how I hire, how I price, how I delegate. Whether or not I ever exit, I’ve already built something worth more than what I had a year ago.

Dylan Carter

Long Term Operator

Academy Member

ABOUT THE FOUNDER

Three exits. One framework. Built for operators like you.

Breakthroughs come faster with the right people around you. The Academy is a curated room of operators who’ve faced what you’re facing.

"Highly recommend this"

The Exit Academy was founded by Mark Botha — author of Built to Exit and creator of the S.C.A.L.E. Framework. Mark didn’t learn this from a textbook. He learned it building, scaling, and selling three businesses.

In 2012, Mark was running a chiropractic practice and selling products on Amazon in his spare time — back when “selling on Amazon” was something most people had never heard of. The side hustle outgrew the practice. He sold the clinic, went full-time into ecommerce, and over the next decade built and exited three businesses — each one teaching him more about what actually moves the needle on valuation, and what wastes a founder’s life.

What he found surprised him: the founders making the most money were often the ones with the least freedom. They’d built jobs, not assets. They had revenue, but nothing a buyer would pay a premium for.

The S.C.A.L.E. Framework was Mark’s answer — the operating system he wished someone had handed him before his first exit. Today it powers Built to Exit, the book read by 225+ founders building toward a sale; SellerVue, the software trusted by 1,200+ ecommerce operators; and the Exit Academy, the private community where founders build businesses that run without them — and sell for what they’re really worth.

If you’re building a commerce business you intend to sell — or one you’d just like to step away from without it falling apart — you’re in the right room.

THE LIBRARY

One mission. Exit on your terms.

A growing library of books for commerce founders. New titles every month.

TO EXIT

THE FRAMEWORK

Built to Exit

Mastering the S.C.A.L.E. Framework to build a business that runs without you — and sells for what it’s really worth. 5.0★ on Amazon

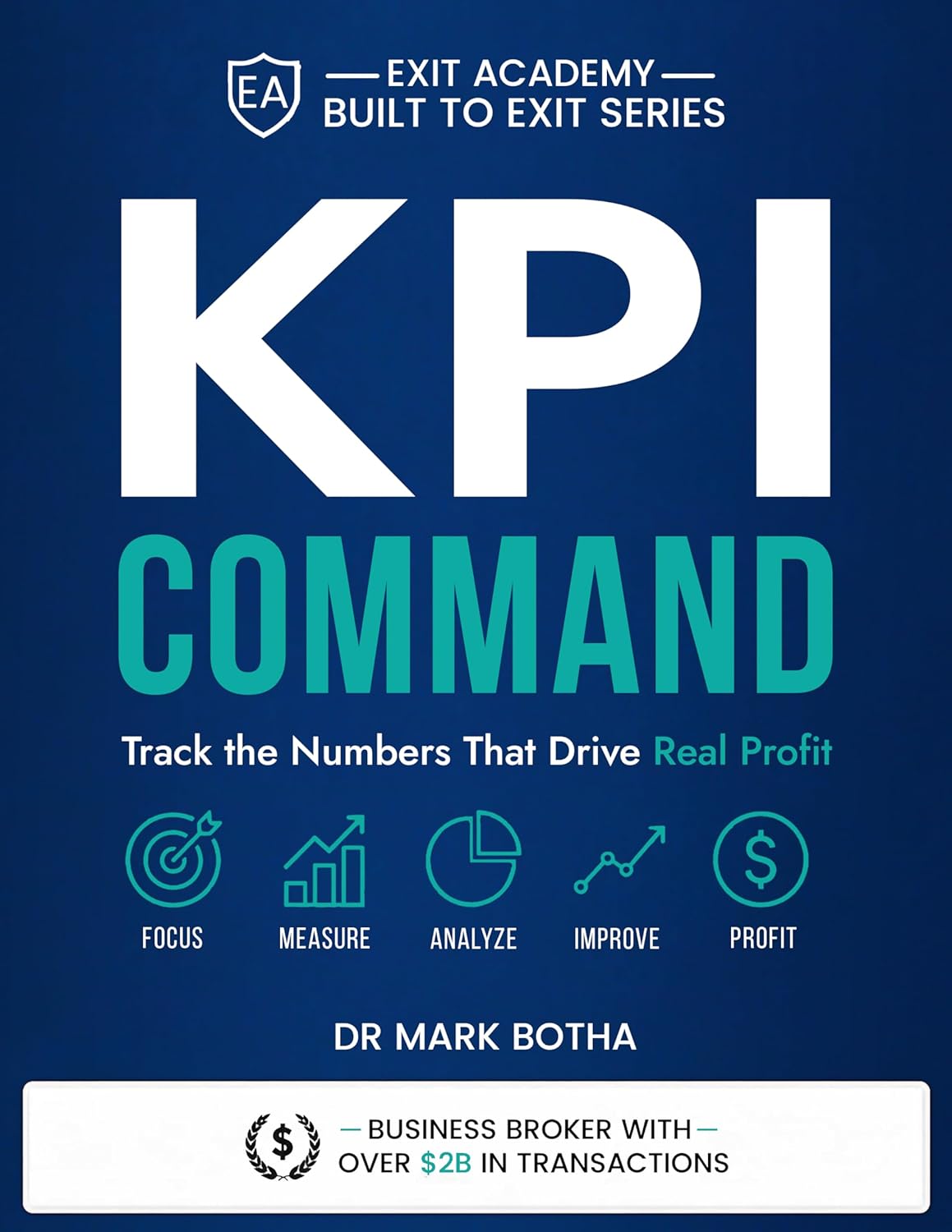

COMMAND

METRICS

KPI Command

Track the numbers that drive real profit.

STORE MGMT

OPERATIONS

E-Com Store Management

The essential systems, processes, and tools behind scalable e-commerce operations.

EXAMINER

MARGINS

Cost Examiner

Find the hidden leaks quietly killing your margins before they cost you growth.

MANIFESTO

EXIT STRATEGY

The Exit Driver Manifesto

The business owner’s blueprint to build, grow, and exit with maximum value.

PLAYBOOK

PROFITABILITY

The Ecommerce Profit Playbook

Simple moves to increase margins and cash flow.

PROOF

MARKETING

Social Proof

Turn trust into more clicks and sales.

STACK

MARGINS

Margin Stack

Build healthier margins across every SKU.

SELLER’S GUIDE

AMAZON OPS

The Ultimate Amazon Seller’s Guide

Accurate landed product costs — the foundation of every Amazon brand that actually makes money.

LEVERS

PROFITABILITY

Value Levers

Increase profit without increasing complexity.

PACK

AI & EXECUTION

Prompt Pack

AI prompts for faster, smarter e-com execution.

THE NEXT MOVE

Stop running the business.

Start owning it.

Revenue is what a job pays you. Equity is what an owner builds. The Academy is where you make the switch — with the systems, numbers, and discipline that turn a business into an asset worth selling.